Example of Credit Reporting Errors

Many consumers believe that once a debt is paid or settled, it will be properly updated on their credit report. However, that is not always what happens.

A case involving Oportun, Inc. highlights how credit reporting errors, inaccurate collection accounts, and failure to update paid debts can continue to harm consumers years after a debt is resolved.

When a Paid Debt Is Still Reported as Unpaid

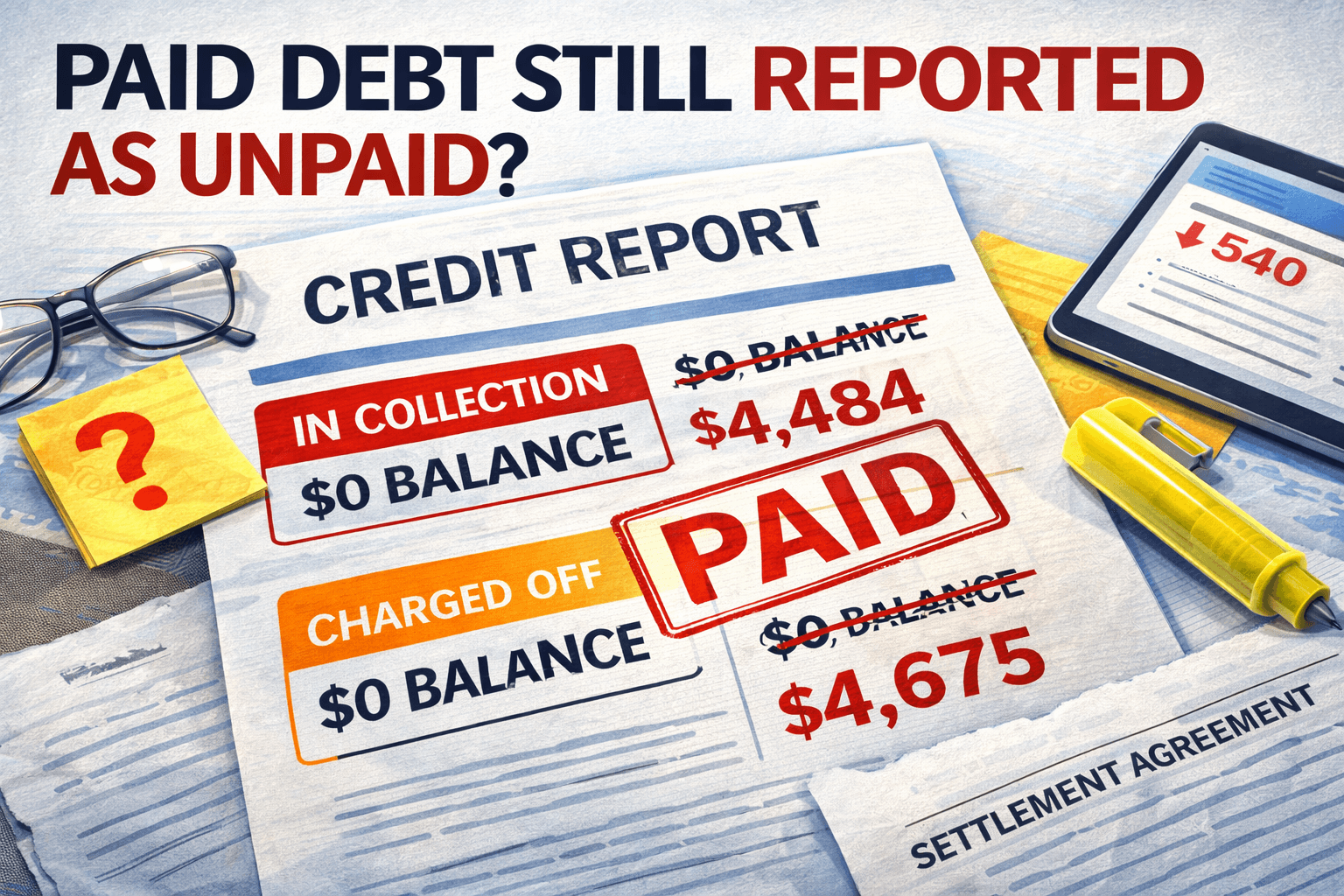

In this case, a consumer had fully resolved two accounts — including a loan and a collection account — years earlier. After settling both, she no longer owed any balance and expected her credit report to reflect a $0 balance.

Despite this, her credit report later showed:

One account still listed as “in collections” with a balance owed

Another account reported as “charged off” with an outstanding balance

This type of issue is commonly searched as:

“paid collection still on credit report”

“why does my credit report show a balance after settlement”

“charged off account still showing balance after payment”

Disputes That Failed to Fix the Problem

The consumer submitted disputes to the credit reporting agencies, explaining that the debts had already been settled and should not be reported with any remaining balance.

However, the credit bureaus failed to correct the inaccurate information, and Oportun, Inc., as the furnisher of the data, did not update the accounts.

This raises a major issue under the Fair Credit Reporting Act (FCRA) — which requires both credit bureaus and furnishers to:

Conduct a reasonable investigation

Review all relevant information

Correct or delete inaccurate data

Why This Type of Credit Reporting Error Matters

When a settled debt is still reported as unpaid, it can seriously damage a consumer’s financial standing.

Common consequences include:

Lower credit scores

Credit denial for loans or credit cards

Higher interest rates

Difficulty qualifying for housing or financing

These situations often lead consumers to search:

“how to remove paid collections from credit report”

“credit report wrong balance after paying debt”

“credit bureau didn’t fix my dispute”

Failure to Update Paid Debts May Violate the Law

Under the FCRA, reporting a balance on a debt that has already been settled may be considered inaccurate or misleading credit reporting.

Additionally, when a consumer disputes the information and it is not properly corrected, it may indicate:

A failure to conduct a reasonable investigation

Continued reporting of inaccurate financial information

Potential liability for both the credit bureaus and the furnisher

In California, consumers may also have additional protections under state law.

What Consumers Should Do If a Paid Debt Is Reported Incorrectly

If your credit report shows a balance on a debt you already paid or settled:

1. Dispute the Account with Credit Bureaus

Clearly explain that the debt has been resolved and the balance is incorrect.

2. Dispute Directly with the Furnisher

Contact the company reporting the account (such as Oportun, Inc.) and request correction.

3. Keep Documentation

Save settlement confirmations, letters, and any communication.

4. Monitor Your Credit Report

Ensure the account is properly updated to reflect a $0 balance.

Bottom Line

This case involving Oportun, Inc. demonstrates a common but serious issue: paid debts that continue to be reported as unpaid.

Consumers should not have to deal with ongoing credit damage after resolving their debts. When credit bureaus and furnishers fail to correct inaccurate information, it may violate federal law.

If your credit report still shows a balance after you paid or settled a debt, and disputes have not fixed the issue, contact The Credit Attorney to review your case and help protect your rights.